Semiconductor industry to undergo a paradigm shift?

Article By : Walden Rhines

The semiconductor industry has shown no consolidation due to its rapidly innovating nature, but after so many decades, isn't consolidation through mergers long overdue?

2015 can be touted as the year of consolidations in the semiconductor industry. Proposed mergers reached as high as $160B in market value and over $100B have already been consummated, making it the largest annual total merger amount in the history of the semiconductor industry.

To many, this consolidation seems natural. After all, the semiconductor industry is now more than sixty years old and the growth rate is slowing, as is common for most maturing industries. Semiconductor sales as a percentage of total electronic equipment sales have been relatively flat for the last twenty years. Consolidation through mergers gradually increases as industries mature so why should the semiconductor industry be any different?

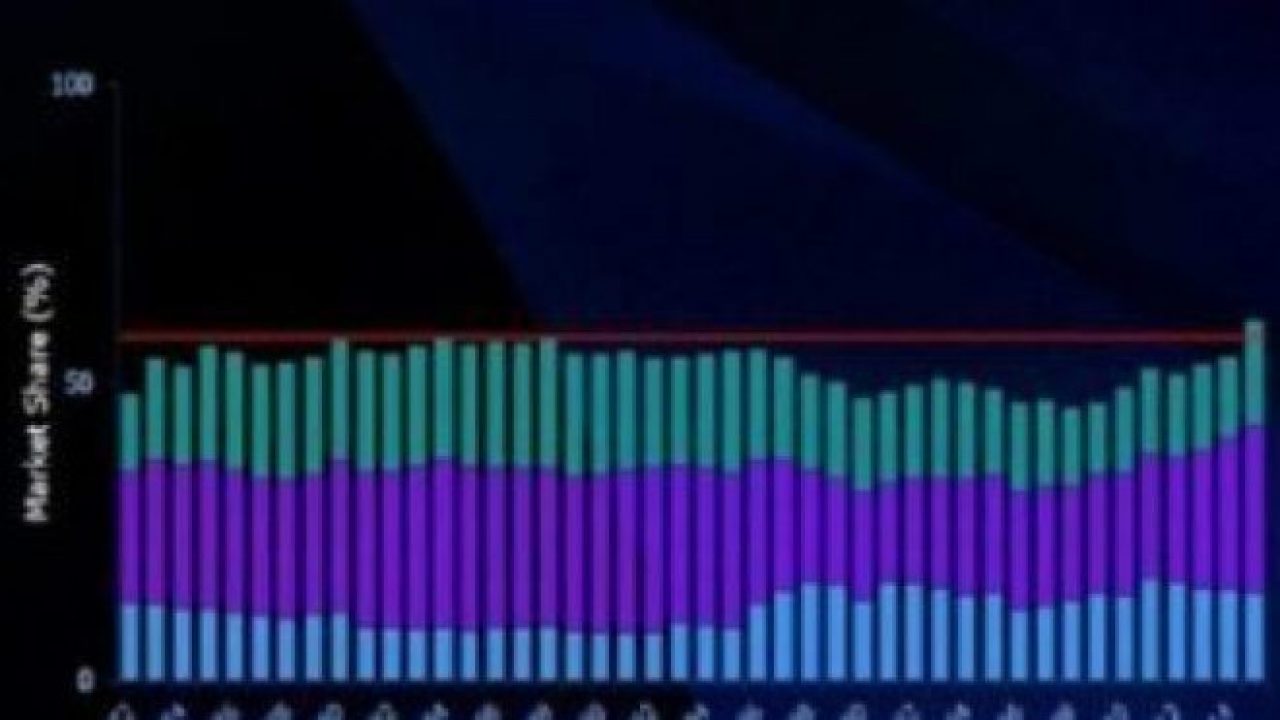

But consolidation is a totally new phenomenon for semiconductors. Because of the rapid innovation that has occurred in the semiconductor industry over many decades, the industry has shown no consolidation through almost all its history. Consider the combined market shares of the largest companies in the industry through 2014 (Figure 1).

![[EEOL 2016MAY20 MFG NT 01]](https://images.contentful.com/455ppwo7h7ge/2ruuHOHsd20Kc4iS6cGuEg/5c109ca72131ca38571b538ed4588795/EEOL_2016MAY20_MFG_NT_01.jpg)

__Figure 1:__ *Combined market share of the top ten semiconductor companies through history.*

Looking back further in history, the semiconductor industry trend has been one of deconsolidation. In 1966, three companies, TI, Fairchild and Motorola, accounted for approximately 70% of the semiconductor industry revenue. By 1972, that combined market share had dropped to 53%. The largest semiconductor company today, Intel, has approximately 15% market share, just 2% more than the number one, Texas Instruments, had in 1972 (Figure 2)

![[EEOL 2016MAY20 MFG NT 01 02]](https://images.contentful.com/455ppwo7h7ge/4gH7s0wiqASquw4ewYAceo/bd5f8750bb54f3ed4059d82ec9388045/EEOL_2016MAY20_MFG_NT_01_02.jpg)

__Figure 2:__ *Overall semiconductor industry has been “DECONSOLIDATING” since the 1960s.*

What about the combined market share of the five largest semiconductor companies? It's been flat for the last 40 years until 2015. Similarly for the top 10. And what about the combined market share of the 50 largest semiconductor companies? It has been steadily decreasing, with a 10 point drop in the last decade (Figure 3).

![[EEOL 2016MAY20 MFG NT 01 03]](https://images.contentful.com/455ppwo7h7ge/3MzXyv6oPKaoOKUyuoqo86/313b75cf3493579102ed53f9eef05d35/EEOL_2016MAY20_MFG_NT_01_03.jpg)

__Figure 3:__ *Top 50 semiconductor company share of market decreased 10 Points in 10 years.*

Although the increase in combined market share of the top 10 companies in 2015 is only 2.5 percentage points above the previous interim high in 1984, this sudden consolidation of semiconductor revenue among a few companies is truly unique (Figure 4). What's different about today versus the last 60 years?

![[EEOL 2016MAY20 MFG NT 01 04]](https://images.contentful.com/455ppwo7h7ge/1bv73kMNWg0OSWaqmsYMYs/28b1f67e471e3a1c53df53d28ec5d798/EEOL_2016MAY20_MFG_NT_01_04.jpg)

__Figure 4:__ *2015 is the first real change in a long term trend.*

Unlike most industries, semiconductors are driven by Moore's Law, effectively doubling the transistor count of the most advanced integrated circuits every two to three years. With that change has come as change in the line-up of semiconductor industry leaders (Figure 5). The top ten semiconductor companies change regularly, with over 50% of the top 10 disappearing from that rank over the last 50 years.

![[EEOL 2016MAY20 MFG NT 01 05]](https://images.contentful.com/455ppwo7h7ge/5KYSjADdtYQYUkAQucoGoe/0868282df9ed2fa841a241e0f78d608f/EEOL_2016MAY20_MFG_NT_01_05.jpg)

__Figure 5:__ *Technology and market discontinuities bring new companies to the top 10.*

Why has all this churn occurred? Each decade is dominated by some new capability for semiconductor technology. The 1950s was a decade of germanium transistor producers who were replaced by producers of silicon transistors. The 1960s were driven by bipolar integrated circuits. The 1970s by MOS memory, 1980s by MOS microprocessors, the 1990s by SoCs with embedded microprocessors and the most recent decades by wireless communications and fabless companies (Figure 5). Each of these decades ushered in new companies that dominated the next wave of technology. Consequently, heroes of previous decades gradually faded until they dropped out of the top ten.

Is it time to declare that the new era for semiconductor consolidation has begun? Maybe. But with only a year or two of data after a consistent trend of more than 60 years, it may be premature. At least it merits an examination of underlying fundamentals that caused 2015, and probably 2016, to reverse such a long term trend. I'll do that in forthcoming articles over the next few months.

—Walden C. Rhines is chairman and CEO of Mentor Graphics. He joined Mentor in 1993 from Texas Instruments (TI) where he was most recently executive vice president in charge of TI’s semiconductor business. Rhines has served five terms as chairman of the Electronic Design Automation Consortium. He is also a board member of the Semiconductor Research Corporation and First Growth Children and Family Charities. He received a BSE degree from the University of Michigan, an MS and PhD from Stanford University, an MBA from Southern Methodist University and Honorary Doctor of Technology degrees from Nottingham Trent University and the University of Florida.

Subscribe to Newsletter

Test Qr code text s ss