ChangXin Emerging as China’s First DRAM Maker

Article By : Junko Yoshida

ChangXin Memory claims it is "China's only DRAM producer" now that it has revved up its fab, which is outputting 20K wafers/month.

SHENZHEN, China — ChangXin Memory (CXMT) has claimed the distinction of being — officially — “China’s only DRAM producer.”

China is boastful of its plan to produce homegrown memory devices, but aside from the NAND flash memory in the works at Yangtze Memory Technologies Co., Ltd. (YMTC) and NOR flash designed by GigaDevice, China has had more ambition than results.

Creating DRAM would be a big step in validating China’s semiconductor ambitions, but industry opinion has been split on whether China can deliver DRAM at all. Even if it does, observers ask how soon China can start shipping commercial DRAMs in meaningful volume.

ChangXin claims to be already doing it. Surprise.

In an exclusive interview with EE Times, representatives of ChangXin Memory (formerly known as Innotron Memory) said the company has completed its Fab 1 and R&D facility in Hefei, the capital of Anhui province, and is currently running 20,000 wafers per month. It is scheduled to double its capacity to 40,000 wafers per month in the second quarter of 2020. Using a 19-nm process technology, ChangXin has begun producing this fall LPDDR4, DDR4 8Gbit DRAM products.

Instead of pursuing the commodity DRAM market, ChangXin has chosen to go after the production of mainstream DRAM.

ChangXin’s emergence as a viable DRAM producer in China is noteworthy, given that several indigenous DRAM vendors have seen their business either stall or die. Worse, Tsinghua Unigroup’s original plans for DRAM production in Nanjing and Chengdu, for example, ended up getting exploited to jack up land prices.

Separating ChangXin from China’s other DRAM production attempts is the fact that ChangXin isn’t just talking the talk. It has actually built a fab, (with expansion plans for two more), while simultaneously building infrastructure to house as many as 3,000 employees and their families in Hefei.

Who’s behind ChangXin?

ChangXin is run by Yiming Zhu, GigaDevice’s former president. It was founded in 2016 by Hefei Industrial Investment Fund and GigaDevice. Technically speaking, the company has no DRAM heritage.

ChangXin also has no association with the Tsinghua Unigroup.

China’s entry into the DRAM market has been tough so far largely for two reasons. First, China has little production experience or expertise. Second, China has not accumulated DRAM-related IP of its own.

So, how does ChangXin getting around such foundational challenges?

Of the 3,000 employees at ChangXin, 70 percent are engineers and technical staff, explained Ian Ng, director of business development at ChangXin.

ChangXin acknowledged that it’s been recruiting engineers from Korea and Taiwan to build its fundamental DRAM knowledge. It has also hired technical staff formerly at Qimonda. These recruits include Karl Heinz Kuesters, who signed on as a “consultant.”

ChangXin views Kuesters as ChangXin’s DRAM ace in the hole. He worked at Qimonda/Infineon for 24 years until Nov. 2008. Kusters was vice president of technology and predevelopment at Qimonda.

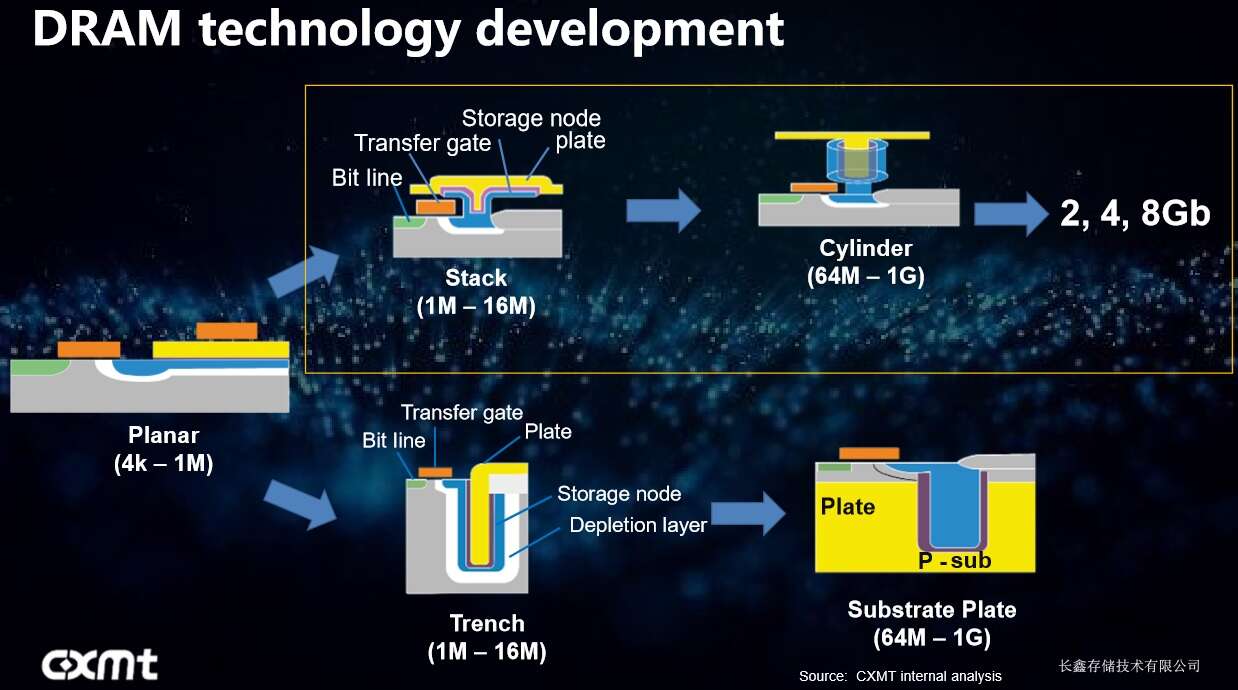

Qimonda’s bailiwick was “trench capacitor” process technology, now regarded as an outdated DRAM technology. When the industry learned that ChangXin was hiring ex-Qimonda people, the assumption followed that ChangXin was using Qimonda’s old trench technology. ChangXin revealed, however, that it has moved into production using “stack capacitor” process technology.

It turns out that Kuesters was responsible for developing Qimonda’s own stack capacitor process technology while he was still there. Qimonda, however, ran out of money before it could transition to stack capacitor.

IP and trade secrets

Hongyu Liu, executive vice president at ChangXin, acknowledged that a tech company, whether it is Qualcomm, Apple, or TSMC, inevitably faces not just IP issues but also the handling of “trade secrets.”

Look no further than Fujian Jinhua. Once viewed as the Chinese DRAM maker with a knack for ramping up yield, Fujian Jinhua today is deemed pretty much “dead.” Fujian Jinhua faced a double whammy, first being accused of stealing trade secrets from Micron, then being put on the entity “blacklist” by the U.S. government.

One memory industry observer based in Silicon Valley, who spoke on condition of anonymity, said, “The operational architecture [of Fujian Jinhua] was pretty smart: Recruit in Taiwan DRAM engineers who don’t want to live in China and then only ship production technology to Jinhua.” He explained, “The only problem is that it recruited too many Micron-Nanya people and some were accused of taking trade-secrets with them. It also doesn’t help that Taiwan is critically dependent on the U.S. for military and political support. So even before the Trump administration, the Taiwan government had complied with a U.S. order to shut down Jinhua Taiwan.”

The nail in the coffin was the U.S. sanctions.

The case, under which the U.S. Commerce Department last year practically banned all exports and technology transfers to Fujian Jinhua, is one of the clearest outcomes yet of Washington’s war on the rise of China’s tech sector. Sanctions by the U.S. and by extension by Taiwan, exacerbated Fujian Jinhua’s shortage of the imported materials to keeping fabrication going.

Liu is not a technologist but an economist by education with a master’s degree from Leibnitz University in Hannover. Having worked for Siemens both in Germany and China for almost 20 years, Liu sees it as her mission to put a proper system in place — including meticulous documentation — at ChangXin so that it upholds higher standards of governance and management.Liu, married to a German executive, speaks fluent German and deftly navigates in two very different cultures. When EE Times asked if she hopes to turn ChangXin into a Chinese company with a German spirit, she smiled and said, “Yes.”

But what about IP? Where is ChangXin getting its IP?

Liu refrained from talking about any definite agreements with IP holders. However, she mentioned WiLAN, a widely known patent troll, now owner of many Qimonda’s patents. WiLAN could be one of the companies with whom ChangXin is negotiating.

To recap: in 2015, WiLAN announced that its wholly-owned subsidiary, Polaris Innovations Limited, acquired from Infineon most of Qimonda’s patent portfolio.

WiLAN noted then that the portfolio included over 7,000 patents and applications, including technologies related to DRAM, Flash memory, semiconductor processes and manufacture, lithography, packaging, semiconductor circuitry and memory interfaces. WiLAN added, “The portfolio has broad relevance to many semiconductor products. The issued patents in the portfolio have an average remaining life of over 8 years. The portfolio includes approximately 5,000 U.S. patents and applications.”

Meanwhile, ChangXin’s Ng noted, separately, that ChangXin has gained access to 10 million know-how documents from Qimonda. Although the rights to these documents are not exclusive to ChangXin, this treasure trove helps the company get a leg up on its rivals, he explained.

With more than 2,000 technical experts already working at ChangXin, Liu made it clear that the company does not plan to rely on the flow of experts from abroad forever. She stressed ChangXin’s focus on “talent development.” She said, “It is our company policy to hire fresh graduates — roughly 500 — every year from universities in China,” in hopes of nurturing future talent locally.

ChangXin in the eyes of analysts

Jim Handy, principal analyst at Object Analysis, views ChangXin as “having a better level of expertise than most people would expect to find in a Chinese DRAM maker.” He described ChangXi as “largely Qimonda’s China design center, but with a shiny new fab thanks to local-government funding.” He added, “This is the same team that briefly produced Qimonda DRAM at SMIC.”

Handy, who has recently released “China’s Memory Ambitions,” has been studying China’s memory growth strategy for several years. Asked about China’s lack of IP and experience/expertise, he explained that China’s DRAM makers can recruit foreign companies already operating in China, or they can recruit Taiwanese, Korean and even Japanese memory experts.

For example, SK Hynix’ Wuxi plant has produced DRAM in China for over a decade, he reminded.

As for IP, Handy said, “This is an issue with most developing nations when they enter semiconductors. Japanese DRAM makers ran into issues with infringing on other companies’ IP in the early 1980s and Korean makers did in the early 1990s. I am sure that China’s manufacturers will work through IP issues but, over the long term, I’m sure that they will work these out in a way acceptable to the developed nations.”

He added, “ChangXin tells me that they have access to all of Qimonda’s IP, which should put them in a more favorable position than other new DRAM and NAND manufacturers in China.”

Brian Matas, vice president of market research at IC Insights, remains more cautious. “We do not believe DRAM production in China is easy and is not moving along as quickly as is often reported. Lack of experience/expertise and lack of IP are definitely two big hurdles.” He noted, “In addition to potentially violating numerous patents, [other issues include] the inability to quickly invest in and transition to new equipment for next-gen process technologies, unable to match the heavy memory R&D spent by Samsung, SK Hynix, and Micron.”

Matas observed, in general, “It is very difficult for an upstart company (or nation) to jump into and grow a DRAM business from scratch that can challenge and keep pace with Samsung, SK Hynix, and Micron. Any gains China can make in DRAM production/output will be lost or left behind as the big three further advance their DRAM devices along the technology curve.”

He concluded, “It is (and will be) extremely difficult for China to build DRAM devices that can be competitive in terms of density, performance, and cost. Delivering substantial quantities of DRAM devices is also a challenge since getting the equipment to produce the devices is very difficult — perhaps akin to the cold war days.”

What happened to Unigroup’s big DRAM plans?

Part of the reasons why some “China hands” remain skeptical of China’s DRAM production plans is because big announcements often turn out to be just “talk.”

In 2017, Chinese media company Sina quoted Zhao Weiguo, chief executive of the Tsinghua Unigroup, saying:

In 2016 we started the construction of the memory base in Wuhan. This year we will build another two semiconductor manufacturing sites in Chengdu and Nanjing. The total investment of the three projects has exceeded $70 billion. Tsinghua Unigroup shoulders the future of IC Industry.

In the end, however, those DRAM fabs in Chengdu and Nanjing have yet to appear.

As IC Insights’ Matas told us, “What we hear about Unigroup and DRAM always includes the word ‘eventually.’” He added, “Don’t think they are doing much now, really don’t see them being a meaningful player in the foreseeable future. They’re making better strides in NAND flash, so that’s likely to remain their area of focus.”

It turns out that prior to joining ChangXin, ChangXin’s executive vice president Liu worked for Tsinghua Unigroup as senior vice president and general manager of IC Fab Build. She confirmed that DRAM production in Chengdu and Nanjing wasn’t happening while she still worked there.

The best explanation came from the anonymous Silicon Valley memory industry source. Speaking of DRAM fab plans in Nanjing and Chengdu, he said, “It’s true that Unigroup tried to solicit local government support to build memories. The financial vision for these city sponsored memory projects was the ex-chairman of Unigroup, Zhao. By planting a memory fab in the city’s science park, the land value automatically goes up. Even if the memory fab fails, the land value alone would make Unigroup very rich.”

He added, “The problem is that neither city wants to eventually fight with Wuhan who is already a Unigroup partner [and making NAND devices]. And at least some of these cities are learning semiconductor capEx is too large and time to profitability is too long. So these all fizzled.”

What kind of DRAM?

ChangXin says that it is focused on mainstream DRAM. What does that entail and who are ChangXin’s competitors?

Handy noted that ChangXin makes LPDDR specifically designed for use in cell phones. He stressed, “If they can make LPDDR, they can make other DRAM, too.”

The fact LPDDR commands a higher price works for ChangXin. But Handy stressed that this strategy, though helpful, is not a big advantage. Because ChangXin is in lower-volume production today, “It makes sense for them to focus on a part that has a higher price. Their cost structure will be higher than it would be for a company making billions of chips.”

The Silicon Valley memory expert shared a slightly more positive take. He noted that Winbond pioneered this field of legacy, small-capacity, industrial, military, satellite-grade DRAM chips. It’s “small volume, high average selling price and neglected markets,” he said. “The problem is, without this market, ChangXin does not have a go-to-market plan. I can’t imagine the specialty DRAM market would be big enough for both Winbond and ChangXin.”

Matas defined specialty memory as being geared to specific applications often consumer mobile applications such as smartphones and tablets.

“Depending on the phone, specialty DRAM for these applications can be high performance, high density, and low-power for maximum battery life. This DRAM can be pricier and is often built using process technology that may be just a step or two behind the very latest,” explained Matas. However, he remained skeptical if ChangXin can match the price and performance of DRAM offered by its competitors.

Subscribe to Newsletter

Test Qr code text s ss