Minimal Transitions, Flat Pricing for Memory in 2020

Article By : Gary Hilson

The 2020 outlook for the memory market looks flat, with transitions doubtful and impact expected from Brexit, trade wars, and the coronavirus.

TORONTO — Will DRAM and flash prices boom again? Will emerging memories finally emerge? Will China’s ambitions begin to pay off? What else is in store for memory technologies in 2020?

The business environment for memory last year was shaped a great deal by low prices for both DRAM and NAND. Jim Handy, principal analyst with Objective Analysis, is expecting the market to be somewhat flat for 2020, with DRAM having endured a significant price collapse that has put a great deal of pressure on margins. Prices may even fall further, he said. “We’re projecting for NAND flash to go up 5% next year. But we’re projecting for DRAM to go down 25%. So, it’s a mixed-up kind of a year. But, when all is said and done, we think 2020 will end with an ongoing oversupply in the memory market.”

Cheap prices for incumbent memories mean there’s not a lot of reason to take a chance on new ones when DRAM and flash are getting the job done at a good price. “They still have a long, tough, hard battle to slog through to get to their place in the front,” said Handy. And with both DRAM and NAND having plenty of runway left based on manufacturers’ road maps, neither is going to run out of speed anytime soon.

Michael Yang, director at IHS Markit, doesn’t see 2020 as the year emerging memories break out either. “There are still hurdles for all these memories.” They are challenged with scaling and bringing costs to a reasonable price point where they can get into more applications, he said, while for the most part, progress on both the DRAM and flash fronts are proceeding per the road maps. Flash, with most suppliers, is gearing up for 128-layer, which is expected, but the ramps for either DRAM or Flash aren’t particularly steep. “The transition to new technology is not as aggressive historically speaking, especially on the DRAM front. Anything new will be very minimally ramped.”

In the middle of emerging memories and the dependable incumbents lays 3D Xpoint technology, primarily in the form of Intel Optane SSDs and DIMMs, as Micron isn’t pushing as hard on the once jointly developed technology. Yang said Intel has been busy getting the word out about the Optane value proposition, “but I think most people are still waiting.” A critical hurdle for Optane is building the ecosystem, he said, not just having customer-ready samples for evaluation, including hardware, software, firmware, and support from the chipset and processors, as well as from the intended applications. “Unfortunately, it is an ecosystem play.”

Yang said Optane is more potentially viable than other emerging memories, and that it is probably ahead in terms of volume, but it still must solve the cost dilemma. “Pricing is a big consideration. You make decisions on what you pay for the performance that you get,” he said. “DRAM prices have come down to very reasonable levels — the price advantage simply got washed away.”

Gregory Wong, principal analyst with Forward Insights, looks at 2019 as an enabling year for Optane, with this year being the first that it’s shipping in meaningful volume, but he also acknowledges pricing is a factor as DRAM prices have plummeted. “We haven’t seen the same for 3D XPoint pricing in terms of cratering.” One variable to consider is that Micron is now shipping a 3D Xpoint SSD, he said, so it’s a wait and see game for a technology that had higher expectations than the traction it has gotten thus far.

While low DRAM prices may curtail Intel Optane DIMM adoption, low 3D NAND prices may impact the SSD adoption. “You’d have to have a really compelling use case to go with that expensive premium when you know NAND is cheap,” said Wong. “And if NAND is really cheap, you might as well just over-provision. There’s a comfort zone there.”

As for other emerging memories, he doesn’t see much happening this year on the ReRAM front as a high-density memory — but more so as a low-power option in embedded applications. Wong sees MRAM having more opportunities in 2020 as a stand-alone, although it has its own inherent challenges. “It doesn’t quite fit in the memory hierarchy.” Today, its performance is lower than DRAM while being more expensive. “You’re basically looking for niches that will accept the high costs because MRAM is potentially a persistent type of memory.”

Not everyone is as optimistic about MRAM. Gill Lee, managing director of memory technology in the semiconductor products group at Applied Materials, said despite the buzz about MRAM potential, there isn’t a huge breakthrough ahead for the technology this year. “MRAM is still mainly pursued as the embedded flash replacement in the micro controller.” He also sees low DRAM and NAND prices inhibiting 3D Xpoint uptake with Intel as the primary driver through its Optane offerings.

Low pricing due to oversupply also tends to mean less capex investment for manufacturing, but Lee said Samsung Electronics’s announcement late last year — that it would make a further $8 billion investment in its memory plant in Xian, China — is a promising one. Further adding to his optimism is that 5G deployments are expected to drive more traffic to the data center. “Data centers are basically the major consumers for memory chips.” (Handy, however, is a little more cautious, because although he sees 5G as a major story this year, part of it is how quickly consumers rush out to buy new handsets.)

However, Lee doesn’t see any major advances ahead from a technology perspective in terms of scaling DRAM and NAND. “Cost effective scaling is the biggest challenge.” The speed of any transition will be closely tied to pricing, he said. “If pricing pressure continues, it will be very challenging to move the node migration. Once node migration happens, the big cost will be scaling, but it still requires capital investment.”

Handy said that need for capital investment could lead to some consolidation in the DRAM space given that the cost of putting up a new fab is growing faster and eating into revenue. “And if we do have outside entrants joining into the market, then that ends up putting more pressure on the existing suppliers to consolidate.”

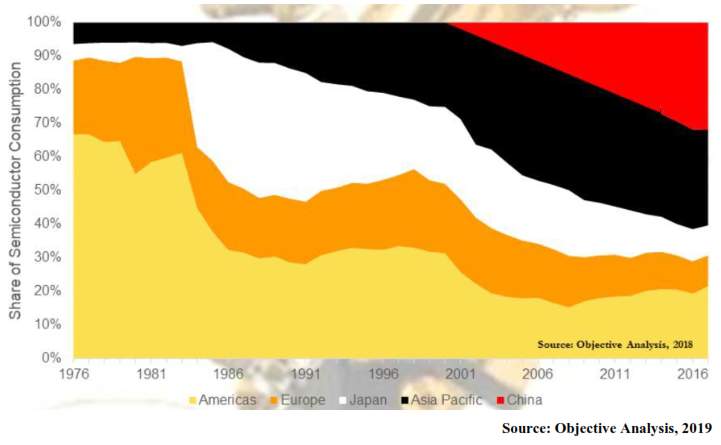

Those new entrants are likely to come from China. Beyond pricing pressures and technology advances, the global economic climate and trade relations will also be key influencers for the memory market over the next year, including China’s role as it looks to build its own capabilities and be less dependent on outside suppliers. IHS’s Yang said regardless of any tariffs, we can expect to see China continue to get stronger as its memory ambitions have been fueled by tensions. “They see this as an absolute must; China is definitely on its way to becoming a stronger player in every market,” he said. “Maybe not in 2020, but definitely I think 2021 and beyond.”

However, at the time of these interviews, the coronavirus was not yet a factor, and it’s already having a short-term economic impact as supply chains are poised for disruption. Brexit and continuing tensions between the U.S. and China will no doubt also continue to be wild cards this year.

Subscribe to Newsletter

Test Qr code text s ss